As the U.S. stock market remains closed for Juneteenth on Monday, investors will be hoping that it doesn’t lose the momentum it built over the past few weeks, as the technology sector carried the market from strength to strength. As of June 16, the S&P 500 was up 14.8 percent this year and 23 percent from its October 2022 low, thus meeting one popular definition of it being in a new bull market.

Ever since that definition of a bull market – an increase of 20 percent from its latest bottom – was first met on June 8, investors have been eager for more, hoping to make up for a disappointing 2022. At the same time, many experts have warned against premature euphoria, raising doubts about whether the current rally can be sustained. Aside from the fact that a recession is still looming over the U.S. economy as the Fed continues to fight inflation, Wall Street commentators have pointed out that this year’s rally has been fueled almost entirely by very few, very large companies.

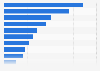

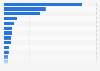

According to Howard Silverblatt, senior index analyst at S&P Dow Jones Indices, the information technology and communication services sectors, i.e. most things tech, were responsible for almost 90 percent of the S&P 500’s year-to-date return as of June 7. Excluding companies from these two sectors, the S&P 500 would have been up just 1.41 percent at the time, instead of 11.98 percent including the tech industry.

Perhaps even more strikingly, just seven out of the 500 companies that comprise the S&P 500 accounted for 84 percent of the index’s year-to-date return as of June 7. According to Silverblatt, Apple, Microsoft and Nvidia alone are responsible for more than half of the index’s gains this year, with Alphabet, Amazon, Meta and Tesla contributing another 34 percent. Taking these companies out of the equation, the S&P 500 would have returned a meager 1.88 percent this year and no one would be talking about a bull market right now.